Licensed Digital Credit Provider | Central Bank of Kenya

Borrow Wisely.

Grow Steadily.Protect Fully.

Grow Steadily.Protect Fully.

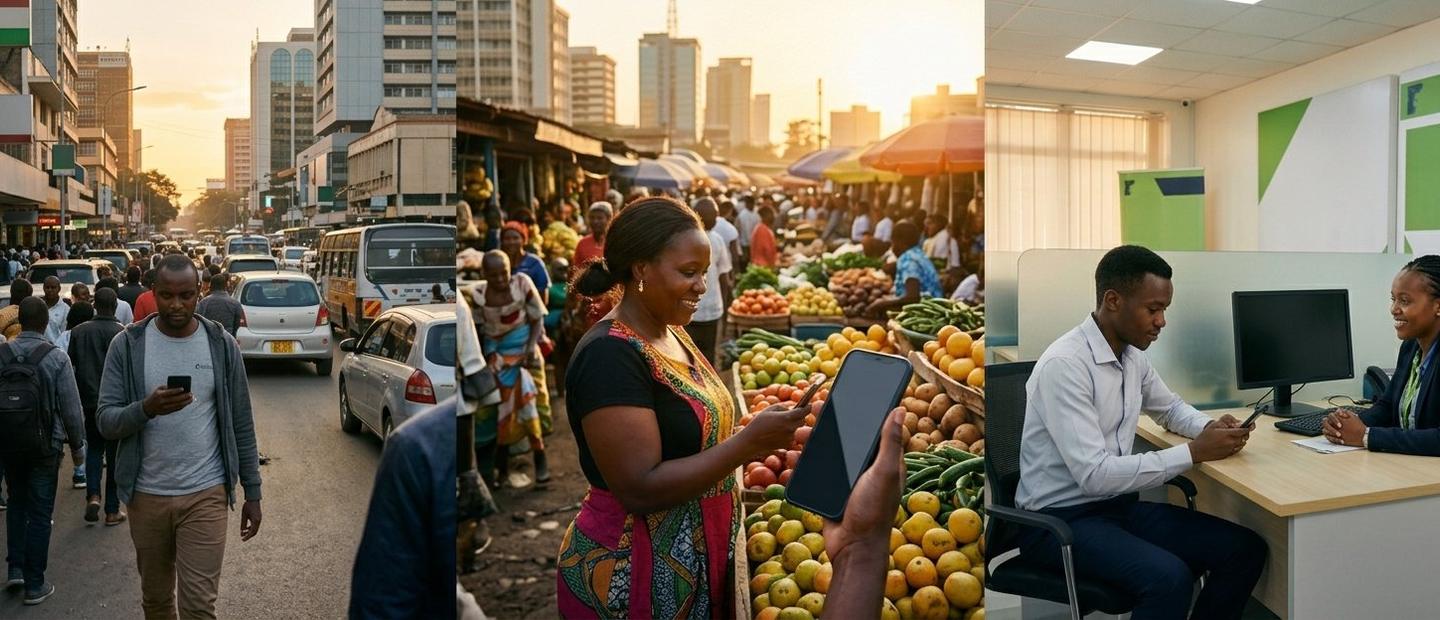

Kenya's inclusive Wealth-Tech ecosystem. We lend responsibly (CBK-licensed DCP) and connect you to licensed fund managers for investments, all to turn every shilling into lasting wealth.

Credit That Builds

Investments That Grow

Protection That Shields